A leaked draft for a European Commission delegated act setting new EU Taxonomy technical screening criteria (TSC) suggests the aviation sector will be included in the EU’s sustainable finance master plan. The leaked document, obtained by French political news website Contexte, follows weeks of speculation that aviation could be dropped from the EU with negative long-term consequences for aviation financing, particularly in Europe Taxonomy (see Insight: ‘Briefing: Aviation EU Taxonomy faces greenwashing accusations’).

Based on Ishka’s analysis of the leaked document (available to download here, see pages 39 - 49), the draft criteria very closely resemble the 30th March 2022 proposal by the Platform on Sustainable Finance (PSF), a working group of the European Commission (see Insight: ‘Ishka's guide to the EU Taxonomy proposal for aircraft leasing’).

Understanding the draft criteria

The leaked draft is set to form the basis of a delegated act, non-legislative acts adopted by the European Commission that serve to amend or supplement non-essential elements of EU legislation, usually those that need regular adaptation to take account of technical progress, such as the EU Taxonomy’s TSC. It covers criteria for transportation sectors that can contribute “substantially to climate change mitigation" and which are yet to be incorporated to the EU Taxonomy, such as aviation.

The draft is not dated apart from the year (2023), but the Commission has been known to be working on this document in recent months. According to a report by European affairs publication Table Europe on 13th March, the delegated act is to be published on 20th March but the aviation passages are still “disputed” within the Commission.

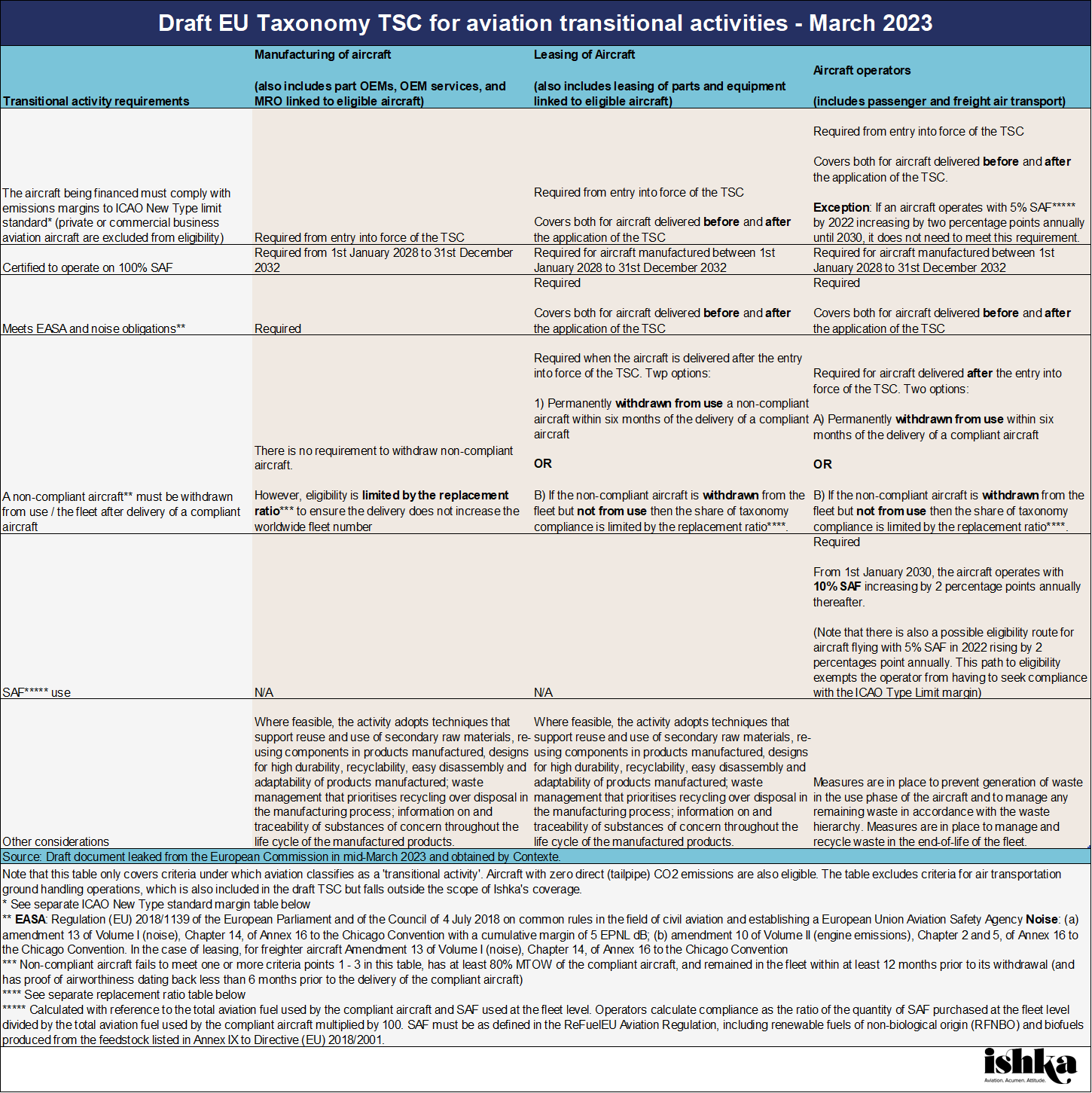

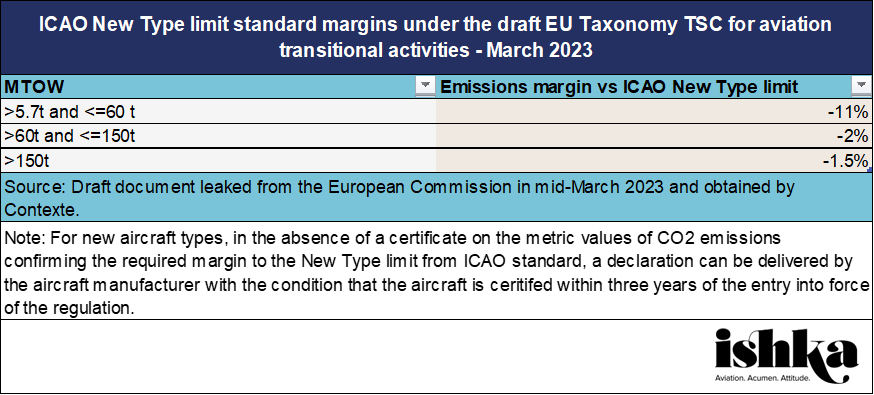

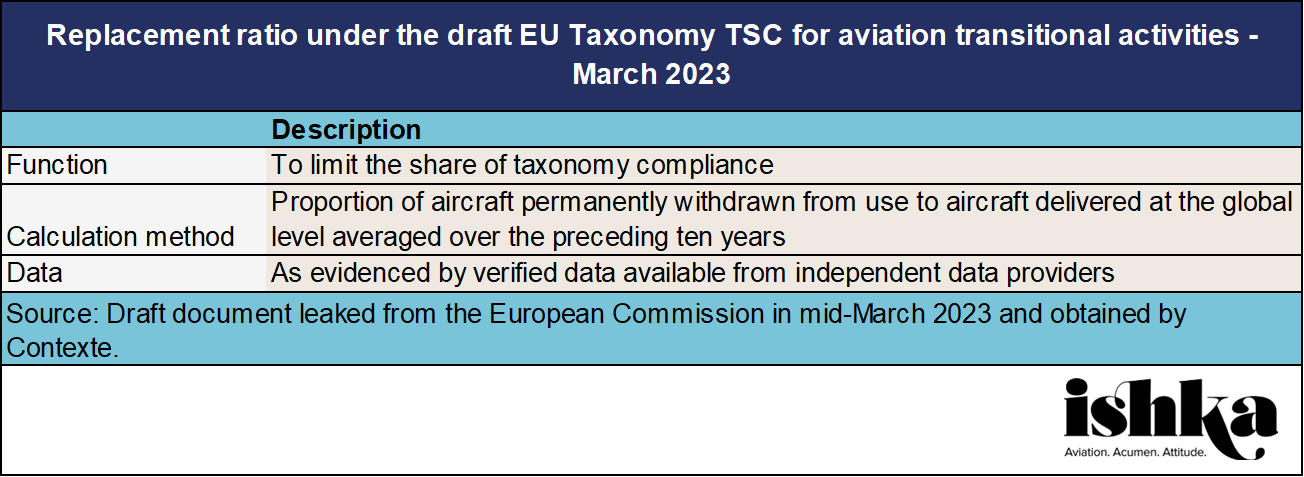

The tables below summarise the criteria for aircraft manufacturing, leasing, and aircraft operators. The ground handling operation sector is also included in the draft but is not analysed as it falls outside the scope of Ishka’s coverage.

Click on the image to see a larger version or Click here to download the tables.

Click here to download the tables.

Differences with the PSF’s 30th March 2022 proposal

The latest draft’s criteria largely resembles the 30th March 2022 PSF proposal – until now the guiding reference for aviation TSC. The main differences include:

- ‘5% + 2% annual’ SAF requirement: For aircraft operators, the PSF proposal included a SAF use requirement of 5% in 2022 (with 2 percentage points added annually), but did not specify whether this would be a parallel requirement or sufficient on its own for an aircraft investment to qualify as a transitional activity. Instead, the European Commission draft allows any aircraft (including those not complying with the ICAO New Type limit standard margins) to obtain EU Taxonomy compliance under the ‘5% + 2% annually’* SAF use target until 2030.

- Ambient air quality: The PSF proposal required compliant aircraft to abide by Directive 2008/50 on ambient air quality, which limits sulfur dioxide, NO2 and other oxides of nitrogen, and particulate matter. The latest draft currently excludes this requirement.

- ‘Best-in-class’ no more – The PSF proposal referred to the ICAO New Type limit standard margins as an aircraft “best in class” criteria. The latest draft no longer refers to these criteria as “best in class.”

- Data sources: The description of the fleet data required to calculate the replacement ratio shifts from “publicly available data (e.g. Cirium)” in the PSF’s proposal, to “verified data available from independent data providers” in the latest draft – no details yet on how it will be verified.

- ‘Decommissioning’ replaces ‘scrapping’: The PSF proposal referred to the need to phase-out older aircraft as a “scrapping rule” whereas the latest draft (DNSH clause 4 – Transition to a circular economy – final paragraph) decommissioning replaces ‘scrappage’. Separately, in points 6.18 (c) (i) and 6.19 (c) (i) of the draft ‘decommissioned’ is replaced by “permanently withdrawn.”

- Private aviation: The PSF differentiated between commercial passenger aircraft and “general aviation” and “business aviation” – the latter two excluded from transitional activity compliance. The latest draft refers to these excluded categories as “private or commercial business aviation.”

- Regular review: The PSF proposal noted that the margins to the ICAO New Type limit standard would be subject to “regular review,” while new criteria for aircraft would be set from 2033. The latest draft makes no direct reference to regular or future review, although several requirements end in 2032, implicitly suggesting a need for revision.

“If correct, the proposals appear to be very similar to the 30th March 2022 Technical Screening Criteria. Some of the contentious terminology such as ‘best in class’ and ‘scrappage’ appear to have been toned down or removed completely,” Barry Moss, President of PACE ESG and Managing Director of aviation ESG risk advisory group AVOCET concurs with Ishka.

* The ‘5% + 2% annually’ SAF use target starting in 2025 is more ambitious than the expected EU-wide SAF blending mandate of 2% by 2025 rising to 6% by 2030. The higher SAF use target aligns with the EU Taxonomy’s role as a pacesetter for the objectives of the EU’s ambitious Green Deal, and therefore it is more ambitious than other policies such as the soon-to-be-finalised SAF mandate (ReFuelEU Aviation).

The Ishka View

The inclusion of aviation criteria in the leaked European Commission draft does not ensure inclusion in the final delegated act, but it goes some way to raise the hopes of aircraft investors and European aviation financiers. While the scrapping (now decommissioning) requirement will pose a challenge for fleet growth-driven airlines and leasing companies seeking taxonomy compliance, it is an important safeguard to prevent Taxonomy-compliant revenue or expenditure resulting in more CO2 emissions. The practical considerations of how this will be implemented remain to be determined.

Environmental groups including Transport & Environment (T&E), the authors of the recent contentious analysis that accused the PSF’s recommended criteria of greenwashing aircraft, are unlikely to be pleased with the leaked draft. On the contrary, it offers reassurance to financial institutions in Europe. In any case, it is worth keeping in mind that the business risks to the final EU Taxonomy criteria of being either too inclusive or too restrictive of assets and transactions are limited: there is no immediate punitive risk for non-compliance. However, that could change in the long term and compliance criteria is likely to be tightened after 2032, if not earlier.

Click on the button below to download the datasheet