in Lessors & Asset managers , Capital Markets , Investor Briefings , Aviation Banks and Lenders

Tuesday 19 June 2018

.png)

.svg.png)

GECAS is first aircraft ABS issuer to use equity asset manager

GECAS’s recent $586.9 million asset backed securitisation, START 2018-1, which has recently priced, is the first air ABS deal to engage an asset manager specifically for the equity portion of the deal. GECAS has engaged OZ Aviation, a Delaware based subsidiary of Och-Ziff a US hedge fund and alternative asset manager, to provide recommendations to the equity directors for the benefit of E noteholders.

The aim is to prepare investors for the eventual sale of the equity portion of the securitisation. For this OZ Aviation will be paid a management fee equal to 0.35% of the portfolio value. Assuming an initial portfolio value of $695,636,756, as reported in the transaction documents, the equity manager’s fee would be $2,434,728.

Source: Bloomberg

As asset manager, OZ Aviation will coordinate updates to the Intex cash-flow model and gather information that will inform its recommendations to the board about aircraft sales opportunities and other portfolio decisions.

The asset manager will be on hand to provide guidance to E note-holders on request and will coordinate with them on any matter relating to consent, instruction, or direction that the E noteholder is required to provide.

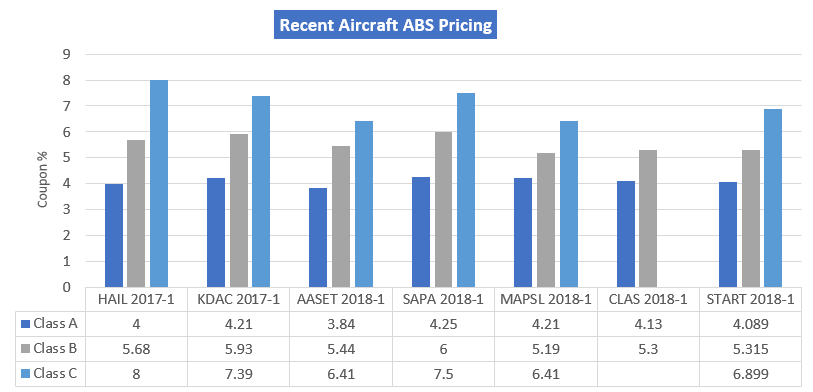

The pricing across A, B, and C note is broadly comparable to recent issuances, see graph below. The first pay date will be 16th of July for investors.

Source: Bloomberg/ Ishka research

The size of the manager’s fee is a possible weakness of the transaction, according to S&P. The transaction’s debt service coverage ratio (DSCR) calculation does not subtract the asset manager’s fee from the available cash. The concern is that the DSCR – 1.15x for the cash sweep, and 1.20x for the cash trap – may be inflated and could delay the triggering of a rapid amortisation event.

Unusually for an aviation ABS the size of the equity portion of the deal has been released. START has issued $100 million in E note certificates. An affiliate of GECAS will retain a small minority of the equity in START 2018-1.

When the E note details are not made public, it is possible to gain a rough approximation of its size by comparing the volume of A, B, and C notes issued, to the initial appraised portfolio value. In theory, the liabilities of the company, debt plus equity, should match the assets of the company, the value aircraft portfolio.

However, as many observers have long suspected, the appraised value of a portfolio is often higher than the actual price paid for the portfolio, which would distort any estimate of the equity size.

For instance, Avolon’s most recent ABS Sapphire Aviation Finance SAPA 2018-1 has an appraised portfolio value of $962,402,401. A notice listed on the Shenzhen Stock Exchange from Avolon’s parent company, Bohai, lists the transaction amount on the 41 aircraft deal as approximately $884 million – a difference of $78.4 million.

In the case of START, based on the equity portion of $100 million, we can infer the actual portfolio value is likely to be slightly lower at $686,900,000, compared to the $695,636,756, reported in the transaction documents.

According to S&P, the portfolio appraisal was conducted one year ago in June 2017. The ratings agency is concerned that the loan to value ratios of the transaction could therefore underestimated. It could also account for the $8.7 million gap highlighted above. For more portfolio information see Ishka Insight: GECAS launches START 2018-1 ABS .

The Ishka View

The use of an equity asset manager is in interesting development in the booming market for aircraft ABS issuances. OZ will likely work with investors to increase the tradability of E-notes. However, S&P has raised concerns over the size of the management fee. The disclosure of the exact size of the equity slice does provide some insight into the true value of the aircraft portfolio compared to the appraised values released publicly.

Sign in to post a comment. If you don't have an account register here.