.png)

.svg.png)

FLY Leasing: all set for an ambitious expansion?

FLY Leasing’s self-proclaimed “transformative” acquisition of AirAsia is looking set to close in Q3 as required approvals come in, overshadowing somewhat Fly’s solid performance in Q1 2018. Ishka sees the logic and the value of the expansion but wonders about the timeline for the lessor’s deleveraging plans.

FLY Leasing is giving itself three years to neutralise the effect of the AirAsia acquisition on its leverage and concentration limits once the aircraft are incorporated into its fleet. Leverage will peak out at 4.9x in year one and descend gradually to 3.5x in year three as aircraft are sold, the lessor has said. Fly targets $150 million in sales in each of 2018 and 2019, and is optimistic the market conditions that have favoured sellers of the aircraft will be supportive of the plan. The equity market’s tepid reaction to Fly’s ambitious expansion plans may be befuddling considering that the industry continues to attract significant capital across the spectrum of the aircraft age. In Ishka’s view, it is likely a combination of nervousness about Fly’s ability to execute a smooth transition to a new business model from both an operational and financing perspectives, and inherent uncertainty about market conditions during a relatively long duration of the transition.

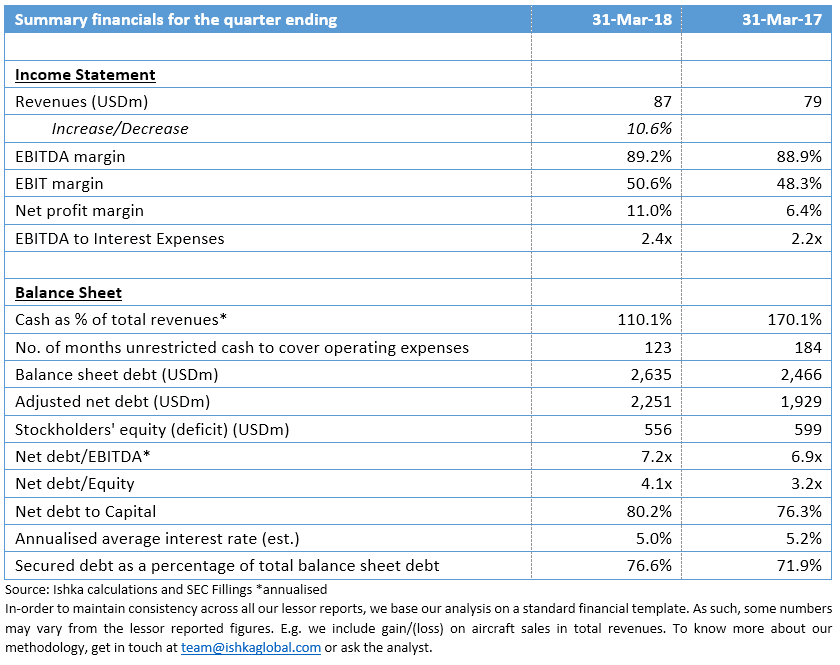

Fly’s acquisition of the AirAsia portfolio has, perhaps inevitably, coloured the discussion of the lessor’s performance since the announcement earlier this year even though the actual deliveries of the portfolio aircraft are not expected until Q2 and are more likely to occur in Q3 2018. The lessor’s Q1 2018 results were positive irrespective of the projected incremental growth, and this should go some way towards demonstrating the fundamental strengths of Fly’s platform. Revenues from operating lease rentals grew by ca. 12% relative to Q1 the year earlier, and the pace of the growth of the cost base was meaningfully lower than the pace of revenue growth (5% versus 12%). The growth in the cost base is attributable primarily to fees relating to the AirAsia deal as well as unrealised foreign exchange losses. Also, directly attributable to the AirAsia deal was the $1.5 million charge taken by Fly for the losses incurred in relation to hedging AirAsia acquisition costs.

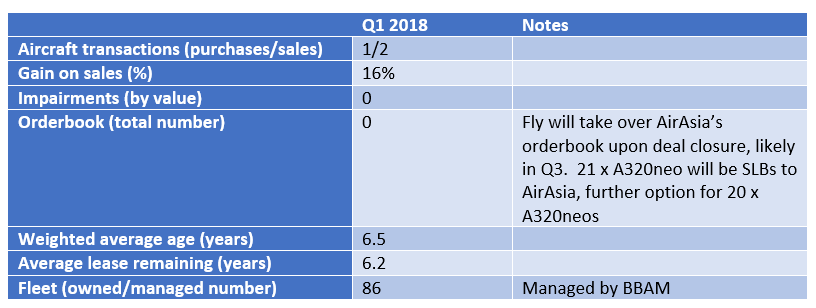

On the operational side, the lessor’s fleet utilisation was 99% in Q1 2018. Fly purchased a new A320 with a 12-year lease attached and disposed of 2 mid-age aircraft, achieving an impressive 16% premium to net book value (the range of gain on sale for the peers, excluding transaction impairments, is mid-single digits to low teens). Fly says there are no further purchases planned for the remainder of 2018 but some capital expenditures are envisaged for 2019 and beyond. On the sales side, none of the incoming AirAsia aircraft are expected to be sold by the end of 2018.

The AirAsia transaction, once approved by all relevant bodies and legally executed, will meaningfully transform Fly’s capital structure. The lessor intends to use $300 million of its cash reserves to finance the deal, in combination with $70 million worth of newly issued equity and $670 million in secured financing (of which $580 million is staple financing at LIBOR+1.725% and $90 million will be drawn from Fly’s acquisition facility at LIBOR+2%). Accommodative pricing suggests debt providers remain highly receptive of aircraft-backed deals, especially on the secured basis. In contrast to many of its peers that have consciously pursued an unsecured financing strategy, Fly is arguing that the “preponderance of secured over unsecured debt” and the overall structure of its debt actually facilitate debt management as it has no balloon payments to contend with.

The Ishka View

Even as the formal completion of the AirAsia acquisition remains all but a foregone conclusion, Fly is lingering in an analyst’s twilight zone—it has metaphorically left one shore but has not yet reached the other. Positive as they were, Q1 results cannot be extrapolated to a future that will bring a vastly different fleet, strategy and capital structure. The expected duration of Fly’s deleveraging may be realistic if the current conditions persist but the changing interest rate environment and rising fuel prices suggest that may not be the case. Notably also, the reported ease with which Fly was able to source secured debt financing for the deal contrasts with the equity market’s stubborn refusal to warm up to Fly’s stock. All of which is to say, Fly has much convincing to do.

Sign in to post a comment. If you don't have an account register here.